Specialist in Asia Pacific, Japan, China, India and South East Asia and Global Emerging Market equities.

Discover moreStewart Investors manage investment portfolios on behalf of our clients over the long term and have held shares in some companies for over 20 years. They launched their first investment strategy in 1988.

Discover more

Please read the following important information for First Sentier Asian Quality Bond Fund

• The Fund invests primarily in debt securities of governments or quasi-government organization in Asia and/or issuers organised, headquartered or having their primary business operations in Asia.

• The Fund’s investments may be concentrated in a single, small number of countries or specific region which may have higher volatility or greater loss of capital than more diversified portfolios.

• The Fund invests in emerging markets which may have increased risks than developed markets including liquidity risk, currency risk/control, political and economic uncertainties, high degree of volatility, settlement risk and custody risk.

• The Fund invests in sovereign debt securities which are exposed to political, social and economic risks. The Fund may also expose to RMB currency and conversion risk.

• The Fund invests in debts or fixed income securities which may be subject to credit, interest rate, currency and credit rating reliability risks which would negatively affect its value. Investment grade securities may be subject to risk of being downgraded and the value of the Fund may be adversely affected. The Fund may invest in below investment grade, unrated debt securities which exposes to greater volatility risk, default risk and price changes due to change in the issuer's creditworthiness.

• The Fund may use FDIs for hedging and efficient portfolio management purposes, which may subject the Fund to additional liquidity, valuation, counterparty and over the counter transaction risks.

• For certain share classes, the Fund may at its discretion pay dividend out of capital or pay fees and expenses out of capital to increase distributable income and effectively a distribution out of capital. This amounts to a return or withdrawal of your original investment or from any capital gains attributable to that, and may result in an immediate decrease of NAV per share.

• It is possible that a part or entire value of your investment could be lost. You should not base your investment decision solely on this document. Please read the offering document including risk factors for details.

A monthly review and outlook of the Asian Quality Bond market.

Market review - as at March 2024

The JP Morgan Asian Credit Index returned a respectable 1.06% amid recalibration in market expectations as investors await more clarity on the Fed’s monetary trajectory. Within the asset class, the investment grade subsector crunched out returns of 0.94% over the month. These positive returns were partially aided by marginally lower US Treasury yields, as well as spreads in investment grade USD Asian credit that continued to inch to record tights, ending the month 5bps tighter at 130bps.

Despite well-known economic headwinds in China, the National People’s Congress (NPC) working group committee announced a 5% GDP growth target for 2024 but maintained deficit target at 3%. While the market welcomed this sign of commitment from Chinese regulators to help the economy recover, skepticism towards the achievability of the growth target without the benefit of low base effects will be a concern. In the technology sector, companies generally saw decent 4Q23 earnings and solid operating cash flow despite investment losses in some names. Lenovo showed some initial recovery with higher year-on-year revenue and quarter-on-quarter improvements in profit margins. CITIC Asset Management Company (AMC) eked out a small profit for financial year 2023 on the back of gains recognized post conversion of China Everbright Bank stake and acquisition of its stake in CITIC Limited, while Cinda AMC reported weaker profit after tax and minority interest. Outside of China, a few South Korean names experienced negative credit rating actions; Moody’s revised LG Chemical’s outlook to negative, while S&P revised its rating outlook on Mirae Asset Securities and Korea Investment & Securities to negative from stable to reflect risks from the companies’ property assets. S&P also downgraded SK innovation to BB+ due to the company’s high capital outlays and subdued battery demand.

Both quasi-sovereigns and sovereigns benefited from the same strong technical momentum that has been pushing spreads in investment grade corporates bonds to tight levels. Spreads in quasi-sovereign names in Indonesia enjoyed a healthy compression particularly in longer dated bonds, outperforming their sovereign counterparts. In HY sovereigns, Sri Lankan bonds had a healthy rally on the back of earlier than expected policy rate cuts as inflation trends began to appear more manageable. Improved economic prospects in Pakistan — easing in inflation, narrowing current account deficit also helped Pakistan bonds advanced up to 10 points higher than the previous month.

Issuance volumes came in stronger than the previous month, though total quantum stayed almost flat. Primary issuance activity was stronger during the second half of the month, with financial names taking the lead. Industrial heavyweight Korea National Oil Corp had the largest issuance with its 3 year, 5 year and floating rate notes amounting to USD1.4billion. In Asian High Yield names, Adani Green Energy and Indiabulls Housing Finance came to the market with ESG bonds.

Fund positioning

Still riding on the momentum in spread tightening, the Fund purchased select Chinese and South Korean names for their attractive yields and participated actively in the primary market, benefiting from names that still offered decent new issuance premiums.

Performance review

On a net-of-fees basis, the First Sentier Asian Quality Bond Fund returned 1.25% in March, outperforming its benchmark by 0.31%.

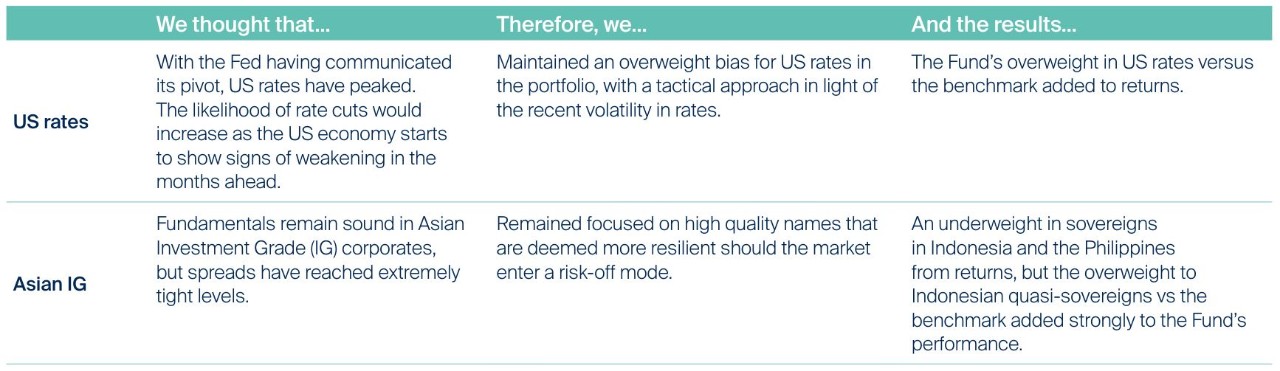

The Fund’s overweight in duration added to performance as Treasury yields move marginally lower over the month. An underweight in sovereign bonds from Indonesia and the Philippines detracted from performance, but this underperformance was more than compensated by the overweight in Indonesian quasi-sovereigns and security selection. Exposure in local currency bonds added to positive returns, but the long position in Japanese yen detracted from performance as the currency weakened in spite of Bank of Japan’s departure from its negative interest rate policy.

Q2 2024 investment outlook

Like how a storyline needs some twists to maintain an interesting narrative, the current market cycle is giving its fair share of suspense as the anticipated easing in the US economy did not materialize over the first quarter of 2024. Recent economic data portrayed US growth to be stronger than expected, with consumption, labor and growth all pointing to resilient broad-based strength in spite of a relatively high interest environment, and inflation still holding up above the Fed’s 2% target.

However, despite the ongoing uncertainty, we do think that the outcome would be largely within expectations, with a slowdown still on the cards. Also, as political noise ramps up in a US election year, we believe that the likelihood of future rate hikes by the Fed is an extremely low probability, even as the timing of rate cuts remains an open question. The path to lower inflation has been noted to be bumpy and we expect global growth, in aggregate, to be slower than in 2023. Given how year-end data can be volatile due to the holiday season, it would be arguably early to conclude that the US is poised to completely avoid a recession. We have witnessed uncertainties and cracks appearing over the past year, and markets can deteriorate very quickly should a downturn emerge. The risk of a stagflation scenario too cannot be totally ruled out and we would rate its probability as higher when compared to the last quarter. Further increases in US treasury issuance, a US debt crisis and a re-acceleration in inflation are possible risks that could challenge the team’s long US duration positioning. Should any of these scenarios pan out, the sanguine outlook that markets have priced in for credit spreads could also be at risk.

In Europe, inflation has mellowed in line with lower energy prices, but growth remains subdued, weighed down by economic heavyweights Germany and France, as well as an overall with pessimism in consumer confidence that has shrouded the region. There is a possibility that the ECB could cut rates earlier than the Fed. We expect the ECB risks not cutting rates soon enough to cushion the effects of the slowdown in growth in the EU.

China’s policies have been turning highly accommodative even though they stop short of a massive stimulus like the one in 2008-2009. In undertaking an ambitious growth target of 5% for 2024, allowing a continued budget deficit of 3%, and issuing special treasury bonds, China is sending a strong signal in committing to growth. However, the multilayered problems causing China’s slowdown means that we don’t expect a quick recovery. The property sector and weak consumer sentiment will remain weak links that need to be addressed. In other words, we still need actual consumer confidence and pre-sales numbers in the property sector to pick up on a sustained basis before market confidence can be restored. Nevertheless, we are of the belief that the Chinese economy will emerge much stronger from this consolidation process and maintain a positive long-term outlook for the economy.

Asian economies have been resilient thus far, but effects from China’s slowdown are not negligible. The growth outlook in Asia is showing signs of weakness especially for export-oriented countries including Singapore, South Korea and Taiwan, caused not only by China’s slowdown, but also reflective of the lackluster demand from developed economies. We believe that this trend is likely to stay. Within the Asian region, countries with a stronger domestic story, such as India and Indonesia, are likely to fare better. Against this weakening external backdrop, most Asian central banks have paused rate hikes as inflation moderated and shifted attention to supporting growth. We remain constructive on the region’s longer-term growth prospects as Asian economies continue to move up the value chain in the global economy.

The Bank of Japan’s (BoJ) exit from its NIRP and YCC policy has not come easy after 17 years in a negative interest rate environment. We expect monetary conditions to remain very accommodative in Japan as the BoJ monitors the long anticipated virtuous cycle — for higher wages to translate into higher spending, for the economy’s ability to sustain inflation at its 2% target. In the meantime, the course of the dollar’s strength remains largely driven by the Fed’s monetary policy. When the first rate cuts are implemented, Asian local currency bonds may perform well, and this will likely lead to further dollar weakness versus Asian currencies, further boosting Asian local bond returns.

While Asian Credit fundamentals have remained stable, demand-supply technicals was the bigger driver of year-to-date performance. In line with broad expectations, the scarcity in bond supply has also rendered new issuance premium to be increasingly small. At this juncture, we remain constructive in Asian IG credit as high all-in yields well above 5% does makes this asset class attractive from an income carry perspective. That said, a risk-off scenario could occur very swiftly at current valuation levels. Our bias is for higher quality names and to ensure sufficient diversification in portfolios as the market rides this rally in credit spreads, with a focus on issuers that have the liquidity and resilience to withstand a hard global landing, should such a scenario emerge.

Source : Company data, First Sentier Investors, as of end of March 2024

Read our latest insights

Important Information

Investment involves risks, past performance is not a guide to future performance. Refer to the offering documents of the respective funds for details, including risk factors. The information contained within this material has been obtained from sources that First Sentier Investors (“FSI”) believes to be reliable and accurate at the time of issue but no representation or warranty, expressed or implied, is made as to the fairness, accuracy or completeness of the information. To the extent permitted by law, neither FSI, nor any of its associates, nor any director, officer or employee accepts any liability whatsoever for any loss arising directly or indirectly from any use of this. It does not constitute investment advice and should not be used as the basis of any investment decision, nor should it be treated as a recommendation for any investment. The information in this material may not be edited and/or reproduced in whole or in part without the prior consent of FSI.

This material is issued by First Sentier Investors (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission in Hong Kong. First Sentier Investors, FSSA Investment Managers, Stewart Investors, RQI Investors and Igneo Infrastructure Partners are the business names of First Sentier Investors (Hong Kong) Limited.

First Sentier Investors (Hong Kong) Limited is part of the investment management business of First Sentier Investors, which is ultimately owned by Mitsubishi UFJ Financial Group, Inc. (“MUFG”), a global financial group. First Sentier Investors includes a number of entities in different jurisdictions.

To the extent permitted by law, MUFG and its subsidiaries are not responsible for any statement or information contained in this material. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment or entity referred to in this material or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

|  |

|---|