Specialist in Asia Pacific, Japan, China, India and South East Asia and Global Emerging Market equities.

Discover moreStewart Investors manage investment portfolios on behalf of our clients over the long term and have held shares in some companies for over 20 years. They launched their first investment strategy in 1988.

Discover more

A monthly review and outlook of the Asian Quality Bond market.

Market review - as at February 2024

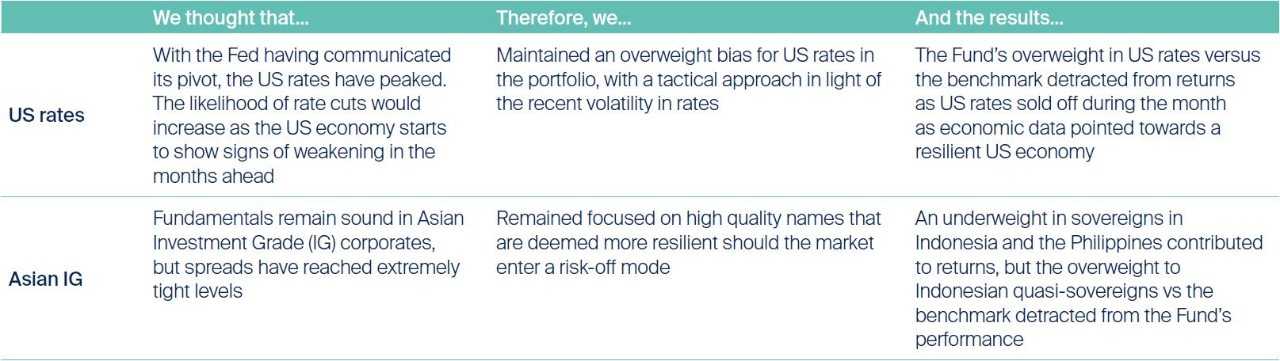

Firmer than expected US economic data pushed US Treasury markets higher during the first half of February. Much of the rates sell-off was buffered by tightening credit spreads, which helped prices remain relatively steady. Nevertheless, USD Asian Investment Grade bonds ended the month marginally underwater with returns of -0.25% even as JACI Asian Investment Grade (IG) credit spreads tightened by 16bps.

Market liquidity was thin in the lead up to the Lunar New Year. Nevertheless, despite the bearish rates environment, strong supply-demand technicals helped Asian Investment Grade bonds to maintain resilience. High beta names’ saw some spread compression. Thailand credit outperformed, with Bangkok Bank and Thai Oil leading the rally. China TMT also tightened by 10-20bps. In Indian credits, the Adani group were the better performers on easing refinancing concerns. Business recovery continued for Macau gaming, and Fitch upgraded Sands China to BBB- from BB+, signifying the Sand China’s transition into investment grade rating category by all three global rating agencies. Late in the month, news circulated about Vanke seeking to extend some non-standard debts and encountering roadblocks in talks with some insurance companies, causing it to be the main underperformer in the Chinese property space. Onshore China sentiment remained poor on the back of the tepid economy and property crackdown, and investors saw China’s onshore equity market sinking to 5-year lows. Chinese regulators then vowed to help stabilize markets and equity markets recovered some lost ground after some buying action by stated-owned institutions and the change in the chairman appointment for the China Securities Regulatory Commission (CSRC).

Spreads in quasi-sovereign names in Indonesia saw mixed performance as longer dated issues experienced low double digits in spread widening due to the sell-off in rates, while shorter dated names went along with the spread compression of the market in general. Outflows in emerging markets added to unfavorable technicals, but fundamentals in the sovereign space remained robust.

The primary market was closed for the Lunar New Year period. In Asian USD Investment Grade credit, issuance was mostly from South Korean names, such as Korea Development Bank’s USD 3 billion dollar issuance.

Fund positioning

After witnessing attractive tightening in spreads, the Fund took profit on select credits while maintaining an overweight in duration positioning relative to its benchmark. Properties exposures were also trimmed slightly on recent price rallies.

Performance review

On a net-of-fees basis (SGD terms), the First Sentier Asian Quality Bond Fund returned -0.74% in February, underperforming its benchmark by -0.35%.

The Fund’s overweight in duration challenged performance as Treasury rates sold off over the month. An underweight in sovereign bonds from Indonesia and the Philippines added to performance, but these returns were eroded by an overweight in Indonesian quasi-sovereigns and security selection. Exposure in local currency bonds and the Japanese yen detracted from performance as the US Dollar strengthened on resilient US economic data.

Q1 2024 investment outlook

2023 has not been for the faint-hearted. The euphoric mood from China’s post-Covid reopening that highlighted the start of 2023 revealed its alter ego as the year progressed with a slew of turbulent events, such as the regional banking crisis and Israel Hamas war. Adding to that, Asian Credit was dealt a challenging hand — the persistent increase in US rates, a struggling Chinese property sector as well as China’s economic slowdown. Thankfully, the resilience of the Asian Credit market came through, with the index as a whole still chalking almost 5% in total returns year-to-date.

Entering 2024, we expect global growth, in aggregate, to be slower than in 2023. Our earlier views that US economic conditions were bleaker than hard data suggested was arguably early, but as Covid-era savings run dry, jobless claims rise and retail sales weaken, we are beginning to see the sobering reality of an economy under strain due to the prolonged high interest rate, high inflation environment. We now expect the Federal Reserve (Fed) to adopt a wait-and-see approach over the next few months before deciding on their next move. Barring a reacceleration of inflation in 2024, we believe the Fed has reached the end of the current rate hike cycle.

In Europe, sustained high prices continue to depress economic growth. Even as headline inflation trends lower, stronger European countries such as Germany are grappling with faltering growth as manufacturing and services activity continue to contract. Unless inflation cools off significantly enough to meet the European Central Bank (ECB’s) 2% target, we expect the ECB risks not cutting rates soon enough to cushion the effects of the slowdown in growth in the EU. We believe that growth in Europe in 2024 would be subdued, at best.

China’s policies have been turning highly accommodative even though they stop short of a massive stimulus like the one in 2008-2009. By allowing budget deficit to widen to above 3%, it is a very strong indication of China’s commitment to prop up growth. However, despite the political commitment to stabilise growth in China, the multilayered problems causing China’s slowdown means that we don’t expect a quick recovery. The property sector and weak consumer sentiment will remain weak links that need to be addressed. In other words, we still need actual gross domestic product (GDP) numbers and pre-sales in the property sector to pick up on a sustained basis before market confidence can be restored. Nevertheless, we are of the belief that the Chinese economy will emerge much stronger from this consolidation process and maintain a positive longterm outlook for the economy.

Asian economies have been resilient thus far, but effects from China’s slowdown are not negligible. The growth outlook in Asia is showing signs of weakness especially for exports oriented countries including Singapore, South Korea and Taiwan, caused not only by China’s slowdown, but also reflective of the lackluster demand from developed economies. We believe that this trend is likely to stay. Within the Asian region, countries with a stronger domestic story, such as India and Indonesia, are likely to fare better. Against this weakening external backdrop, most Asian central banks have paused rate hikes as inflation moderated and shifted attention to supporting growth. We remain constructive on the region’s longer-term growth prospects as Asian economies continue to move up the value chain in the global economy.

Thus far, the rising inflation in Japan has been insufficient to convince Japanese regulators to normalise monetary policy. However, the Bank of Japan’s next move should be closely watched as any signs of change to their Yield Curve Control policy will have significant implications for the course the dollar’s strength. We see higher certainty of the Euro and other Asian currencies continuing its appreciation against the US dollar, a trend that is largely driven by the Fed’s move. Asian local currency bonds may perform well should the Fed cut interest rates in 2024, as this will likely lead to further dollar weakness versus Asian currencies, further boosting Asian local bond returns.

We remain constructive in Asian IG credit. Fundamentals are now mixed but technicals will likely remain a tailwind during the early part of 2024. Even as credit spreads are almost at postGFC tights, high all-in yields well above 5% does makes this asset class attractive from an income carry perspective. Our bias is to focus on higher quality names that have the liquidity and resilience to withstand a hard global landing, should such a scenario emerge.

Source : Company data, First Sentier Investors, as of 29 February 2024

Read our latest insights

Important Information

This material is prepared by First Sentier Investors (Singapore) (“FSI”) (Co. Reg No. 196900420D.) whose views and opinions expressed or implied in the material are subject to change without notice. To the extent permitted by law, FSI accepts no liability whatsoever for any loss, whether direct or indirect, arising from any use of or reliance on this material. This material is published for general information and general circulation only and does not have any regard to the specific investment objectives, financial situation and particular needs of any specific person who may receive this material. Investors may wish to seek advice from a financial adviser and should read the Prospectus, available from First Sentier Investors (Singapore) or any of our Distributors before deciding to subscribe for the Fund. In the event that the investor chooses not to seek advice from a financial adviser, he should consider carefully whether the Fund in question is suitable for him. Past performance of the Fund or the Manager, and any economic and market trends or forecast, are not indicative of the future or likely performance of the Fund or the Manager. The value of units in the Fund, and any income accruing to the units from the Fund, may fall as well as rise. Investors should note that their investment is exposed to fluctuations in exchange rates if the base currency of the Fund and/or underlying investment is different from the currency of your investment. Units are not available to US persons.

Applications for units of the Fund must be made on the application forms accompanying the prospectus. Investments in unit trusts are not obligations of, deposits in, or guaranteed or insured by First Sentier Investors (Singapore), and are subject to risks, including the possible loss of the principal amount invested.

Reference to specific securities (if any) is included for the purpose of illustration only and should not be construed as a recommendation to buy or sell the same. All securities mentioned herein may or may not form part of the holdings of FSI’s portfolios at a certain point in time, and the holdings may change over time.

In the event of discrepancies between the marketing materials and the Prospectus, the Prospectus shall prevail.

In Singapore, this material is issued by First Sentier Investors (Singapore) whose company registration number is 196900420D. This advertisement or material has not been reviewed by the Monetary Authority of Singapore First Sentier Investors (registration number 53236800B), FSSA Investment Managers (registration number 53314080C), Stewart Investors (registration number 53310114W), RQI Investors (registration number 53472532E) and Igneo Infrastructure Partners (registration number 53447928J) are the business divisions of First Sentier Investors (Singapore).

First Sentier Investors (Singapore) is part of the investment management business of First Sentier Investors, which is ultimately owned by Mitsubishi UFJ Financial Group, Inc. (“MUFG”), a global financial group. First Sentier Investors includes a number of entities in different jurisdictions..

MUFG and its subsidiaries are not responsible for any statement or information contained in this material. Neither MUFG nor any of its subsidiaries guarantee the performance of any investment or entity referred to in this material or the repayment of capital. Any investments referred to are not deposits or other liabilities of MUFG or its subsidiaries, and are subject to investment risk, including loss of income and capital invested.

|  |

|---|